Click here for Japanese version (日本語版はこちら)

Note: In Japanese, the word “ABEKOBE” means to reverse or confuse the order, so I used the word “ABECOMICS” for expressing that “ABENOMICS” has recently seemed to deploy economic policy without the order or scenario that should be.

This is the 4th time of the entries which are titled with “ABENOMICS”.

At the first, I pointed out some misreading of public opinions about it, and I guessed that its essence was regarded as something like the “traditional conservative”, rather than like the “neoliberalism”. At the second which picked up the “growth strategy”, I mentioned about its contemporary meaning from the viewpoint different from general opinions and pointed out the importance of “a clean break from the past” just like opening the “Pandora’s box”. At the last time, picking up an issue about the consumption tax hike, I pointed out a cloud such as limits of thought like the “growth pole and trickle-down” in the economic indicators that seemed to be relatively stable at that time, and speculated that it might become their crossroads.

If they are regarded as “KISHOTENKETSU” which is the four‐part (introduction, development, turn and conclusion) organization of Chinese poetry, this time will become its conclusion.

Thinking of recent little slump of markets such as the stock exchange, one of turning points of the ABENOMICS seems to have just come. It has passed about one year and more since the newly monetary easing measure by Mr. Kuroda, but booms of markets seem not to be able to continue only by something like expectation.

When things cannot go well, there are often mistakes in issues themselves or their preconditions. Can we really say that there is nothing like that in common sense of our macroeconomic management?

An antithesis to Macroeconomic Management

Looking back economic history for a while, the welfare state of Keynesian had reached dead end in 60-70’s by the stagflation triggered by twice oil shocks. However, even if being drawn into its vortex, they say that people seemed to have an illusion of having overcome a fate of business cycle.

Today’s situation is resembled to that. After the deadlock of aggregate demand management mainly by fiscal policy, financial policy has become to be emphasized among macroeconomic policy in 80-90s. At the same time, so-called “monetarism” had come to the fore of neoclassical, and also a part of Keynesian thought out the “Mandel-Fleming Model”.

Such macroeconomic management seemed to have reached its peak when it was called “new economy” by the former FRB chairman though the IT bubbles collapsed after that. In fact, U.S. economy of those days had often been praised, for example, “We have just overcome a fate of business cycle after all” and so on.

However, the series of financial crisis such as the subprime loan problem, the failure of Lehman Brothers, and the Euro Crisis proved that such “common sense” was just something like haughtiness. That looks like saying that the method inflating effective demand artificially and politically isn’t a sustainable approach for macroeconomic management, in spite whether it’s fiscal or monetary policy.

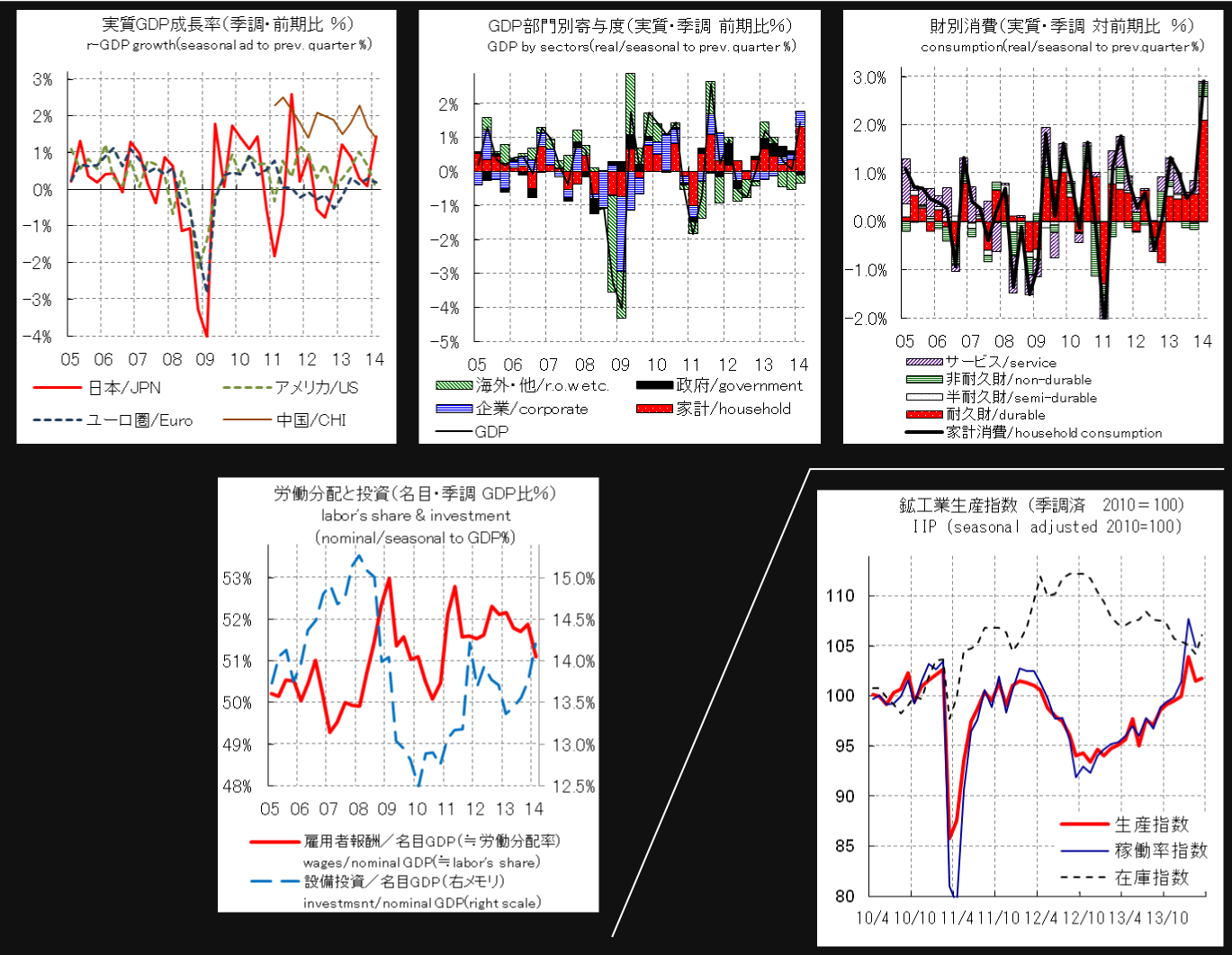

In our country, while being beside of the financial crisis of western countries or slowdown of emerging countries’ growth, “gradual recovery” has supported by domestic demand. Not a small part of it has been contributed by the household demand, and it may owe a lot to optional consumption, thinking of relatively high increase of durable goods and services.

It’s not difficult to guess that almost of these has been supported by asset effects due to the “Kuroda’s monetary easing”. Therefore, a recent slump of markets including the Tokyo stock exchange may become more crucial factor of business climate than many experts are thinking. Moreover, unexpected growth of the 1st quarter GDP of 2014 seems to owe a lot to a last-minute rush in association with the consumption tax hike. That’s why the household income such as a labor share has not improved while availability of equipment increased dramatically under this relatively high growth.

The more unexpected rush will bring the more a reaction as reduction…It might be enough as a trigger of slump of domestic economy.