Click here for Japanese version

日本語版はこちら

I’ve personally sorted out economic indices every time when quarterly GDP is released, so I’m going to publish it on this blog from now on.

GDP in 1st quarter of 2013 increased at a seasonally adjusted annual rate of 3.5% in real terms. It was relatively high growth, and its summary and a part of related indices is as some sheets below.

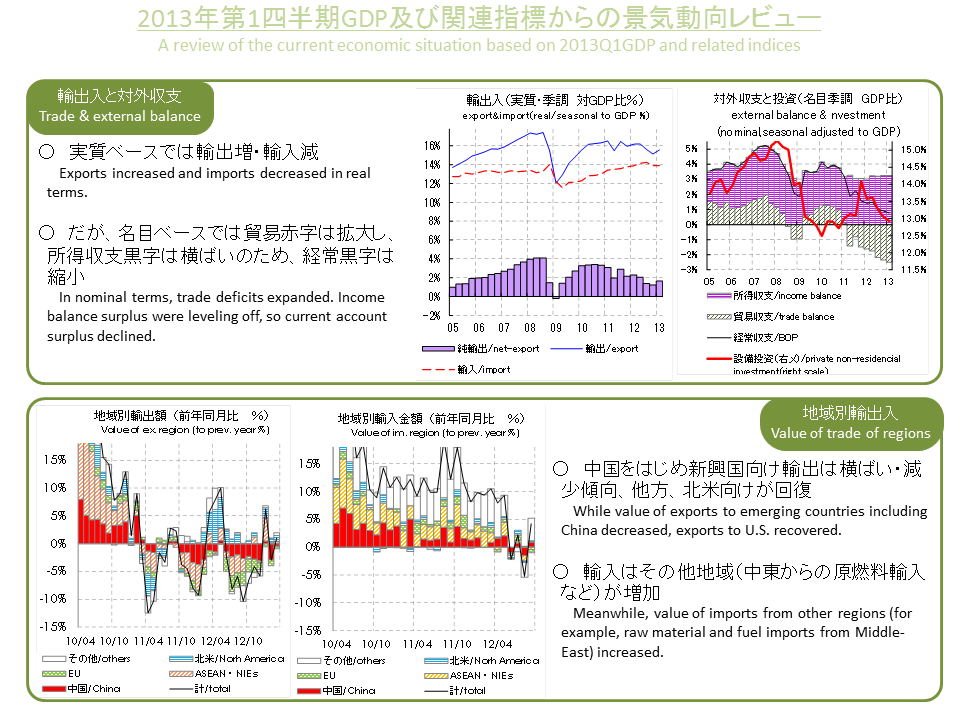

One of factors of this recovery is the rest of the world sector, and its driving force had shifted from Asia to U.S. In the background of this, there was slowdown of Asian economies, which had been driven by external demand, triggered by the Euro Crisis as I wrote at some entries such as “The Creditors Dilemma” or “The China Crisis“.

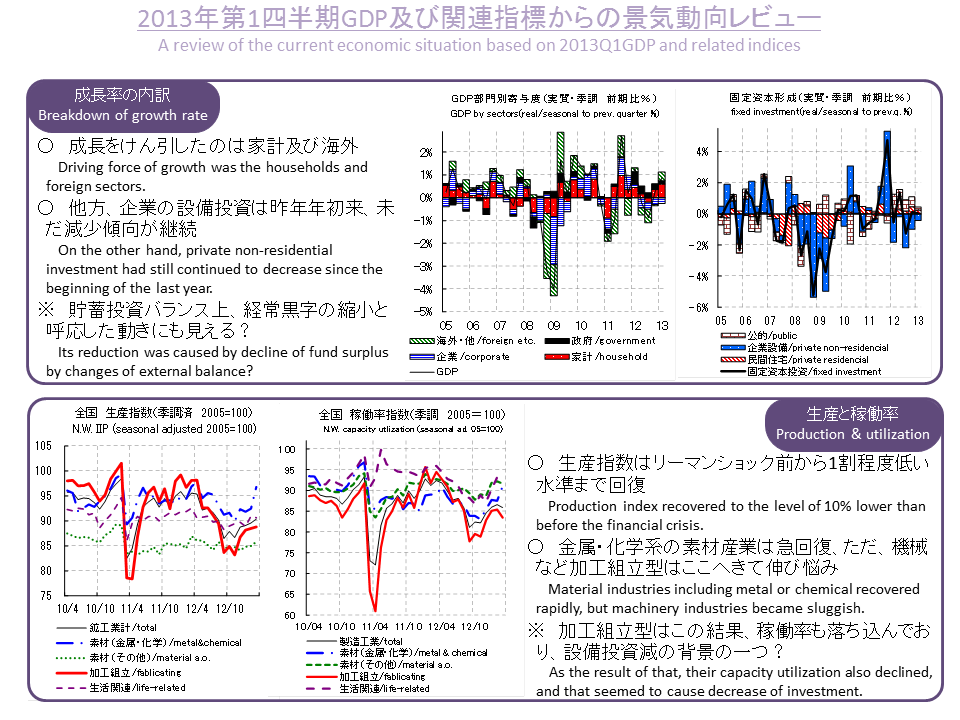

Another factor of this recovery was consumption of the household sector, but it seems that it was contributed by rather service consumption than durable goods consumption which had driven domestic economy for a long time due to various subsidies.

In contrast to these, investment of the corporate sector was relatively inactive. There were some reasons, but the most obvious factor may be decline of capacity utilization, especially machinery industries due to Asian slowdown. However, if thinking furthermore, we may have to take other factors such as the relation between price level and labor’s share, or the changes of investment-savings balance due to the changes of external balance into account.

Among these, from a view of the former (income distribution), we can see a trend that is shrinking of investment while maintaining employment income under downside pressure by deflation for this half an year. This point is consistent to the coexistence of both of “steady households” and “sluggish corporate” in expenditure terms.

(To enlarge sheets below, please click anything you want.)

By the way, these are indices just till March, and this country’s economic atmosphere has changed completely since then as you know.

With that in mind, I’m going to suggest two points that will become key factors from now.

One of these is an issue about price levels and labor’s share which has often been pointed out.

Needless to say, pulling out of deflation must get into step with increase of wages. If the timing is wrong, domestic demand will shrink more through deterioration of corporate profits in addition to employment income.

In short, it can be said that success or failure of macroeconomic policies is always depend on a problem about strategy, order or scenarios… It’s the fact that they’ve gone well since the beginning of their regime change, but it’s unknown whether they will be able to keep it furthermore if people come out of expectation that has exceeded economic performance.

In fact, by the stock market crash of the day before yesterday, we were forced to remember that economy just supported by expectation is commonly associated with huge risks. Although the matter of China slowdown was already obvious as I wrote before less than a year, a harmful effect of “the portfolio rebalance policies”, which is decline of liquidity of the government bond market by “freeze-out” of private money, seems to be kind of little miscalculation.

Perhaps, economic evaluation axes of people and markets will shift from just expectation to real performance after this incident.

Another point is an issue of the meaning of existence of nations and regions from a view of economic resource allocation in this era of globalization.

As mentioned above, trends and insights viewed from GDP statistics has changed for only this 3 or 6 months completely. It has gone like that for this lost 20 years, and it will become more so from now. There is not any assurance of future growth of today’s “growing” sector, and there is often possibility that it has ended when we’ve decided.

Flexibility based on diversity is only a way to cope with various changes because it will be able to treat any problem. Today’s raison d’être of nations and regions is very this point, in short, it’s just like risk sharing among people with skills and abilities of various levels as I wrote the other day.

Among their policies which has been taken just now such as trade liberalization or domestic deregulation, some will increase the possibility of the risk sharing, and others will not do so. That will depend on concrete operation because these are only things like systems or environments.

After the financial crisis, we should already know that kind of markets is not more effective than we have thought and also it’s often something like fence-sitting and self-fulfilling. Their ultimate mission may be to control harmful effects of market mechanism without sacrificing its advantages.

As I mentioned on the entry “A Fate of ABENOMICS” at the beginning of this year, they are rather discretion-oriented just like their words “New Targeting Policy” than market-oriented about economic resource allocation. Will they be able to find out a solution of the mission?

Probably, its answer will be unraveled in the not too distant future.

Pingback: The crossroad of Abenomics by a consumption tax issue / A review about GDP statistics of Q2-2013 | Imbalance & Rebalance

Pingback: ABENOMICS becoming like “ABECOMICS”/ Isn’t it the road they have already experienced? | Imbalance & Rebalance